If you’ve been thinking about buying a home, you likely have one question on the top of your mind: should I buy right now, or should I wait? While no one can answer that question for you, here’s some information that could help you make your decision.

Do You Need a House?

This is an important consideration. If you are in need of a new house, then yes, now is the time for you to buy. Whether your landlord is selling your rental, you’re relocating for a new job, or your current home just doesn’t meet your needs, the best time to buy is when you are actually in need of a new home.

Why Should I Buy Right Now?

There’s a variety of reasons that make it a good time to buy right now, despite what you may hear.

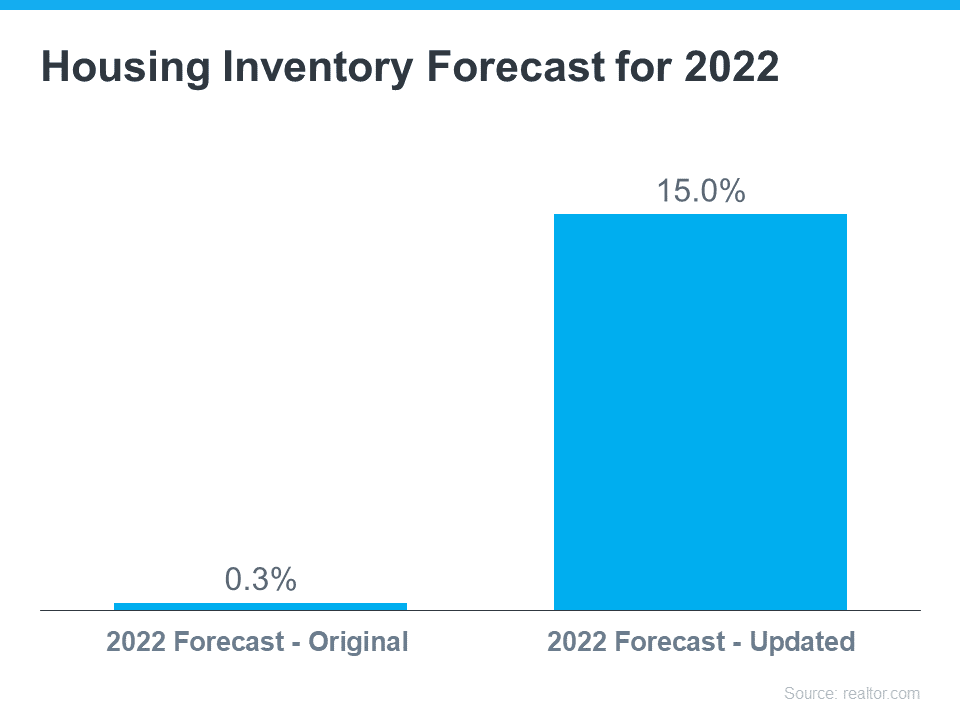

The Supply of Homes for Sale Projected To Continue Increasing

This year, particularly this spring, the number of homes for sale has grown. That’s partly due to more homeowners listing their houses, but also because higher mortgage rates have helped ease the intensity of buyer demand. Moderating buyer demand slows down the pace of home sales, which in turn helps inventory rise.

Experts say that growth will continue. Recently, realtor.com updated their 2022 inventory forecast. In the latest release, they increased their projections for inventory gains dramatically, going from a 0.3% increase at the beginning of the year to a 15.0% jump by the end of 2022 (see graph below):

More homes to choose from is great news if you’re craving more options for your home search – just know that there isn’t a sudden surplus of inventory on the horizon. Housing supply is still low, so you’ll need to partner with an agent to stay on top of what’s available in your market and move fast when you find “the one”. It’s not going to be easy to find a home, but it certainly won’t be as difficult as it has been over the past two years. During the last two years, quite a few buyers had to settle because there just weren’t very many options, especially at certain price points.

With this increase in inventory comes an advantage for those who have less cash or those using a VA or FHA loan. During the height of the “frenzy”, many buyers were offering all cash, substantial appraisal gaps, or large amounts of money down. This meant any VA, FHA, or offer without an escalation clause/appraisal gap would be at the bottom of the pile, if considered at all.

Should I wait for prices to go down?

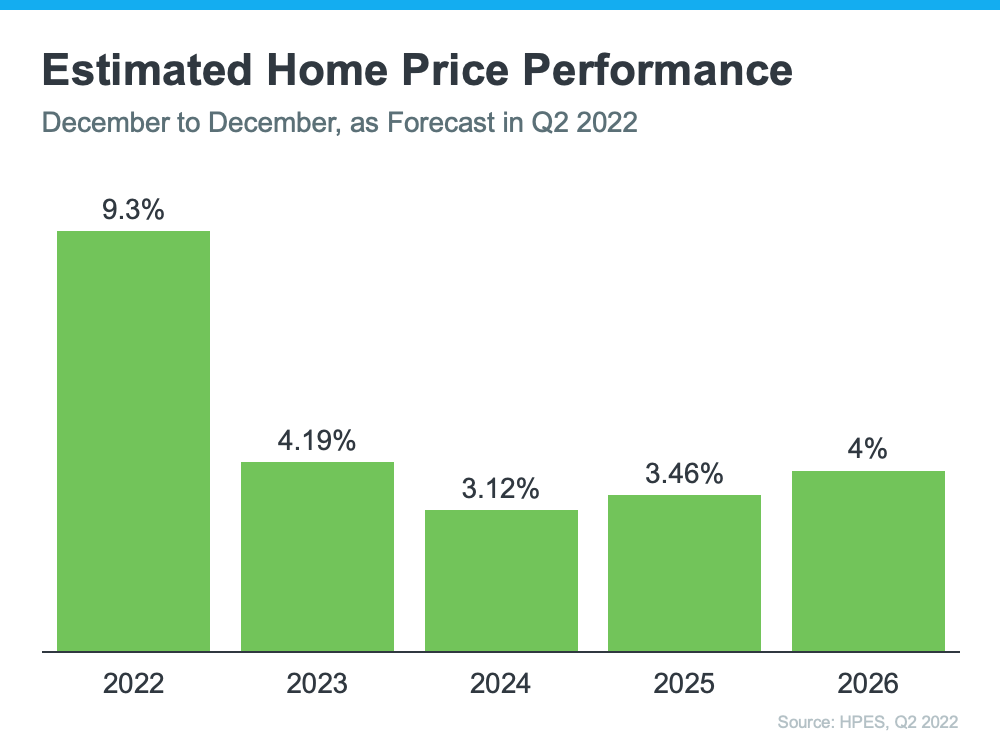

Each quarter, Pulsenomics surveys a national panel of over 100 economists, real estate experts, and investment and market strategists to compile projections for the future of home price appreciation. The output is the Home Price Expectation Survey. In the latest release, it forecasts home prices will continue appreciating over the next five years (see graph below):

As the graph shows, the rate of appreciation will moderate over the next few years as the market shifts away from the unsustainable pace it saw during the pandemic. After this year, experts project home price appreciation will continue, but at levels that are more typical for the market. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

People should not anticipate another double-digit price appreciation. Those days are over. . . . We may return to more normal price appreciation of 4%, 5% a year.

For you, that ongoing appreciation should give you peace of mind that your investment in homeownership is worthwhile because you’re buying an asset that’s projected to grow in value in the years ahead.

But waiting for prices to go down, well, that will cost you. It is a gamble and economists agree that homes will continue to appreciate, just at a much more moderate level. Couple increasing prices with increased interest rates, and that same home will cost you more next year.

But What About Interest Rates?

High interest rates should not completely deter you. We have some awesome programs to help you lower your rate, even if temporarily, to get you into a home. Not to mention that refinancing to get a lower rate is always an option later down the road should rates lower significantly. However, waiting for interest rates to lower will end up costing you even more as home prices continue to rise. Locking in a lower overall home price, with the option to refinance later, could be the smarter option.

It’s also important to note that the drastically low rates from the pandemic era were meant to stimulate the economy, and not meant to be long-term. The rise in interest rates certainly can impact purchasing power, but our current rates are still really good considering where we have seen them in the past few decades.

What About Inflation?

Real estate is a great investment

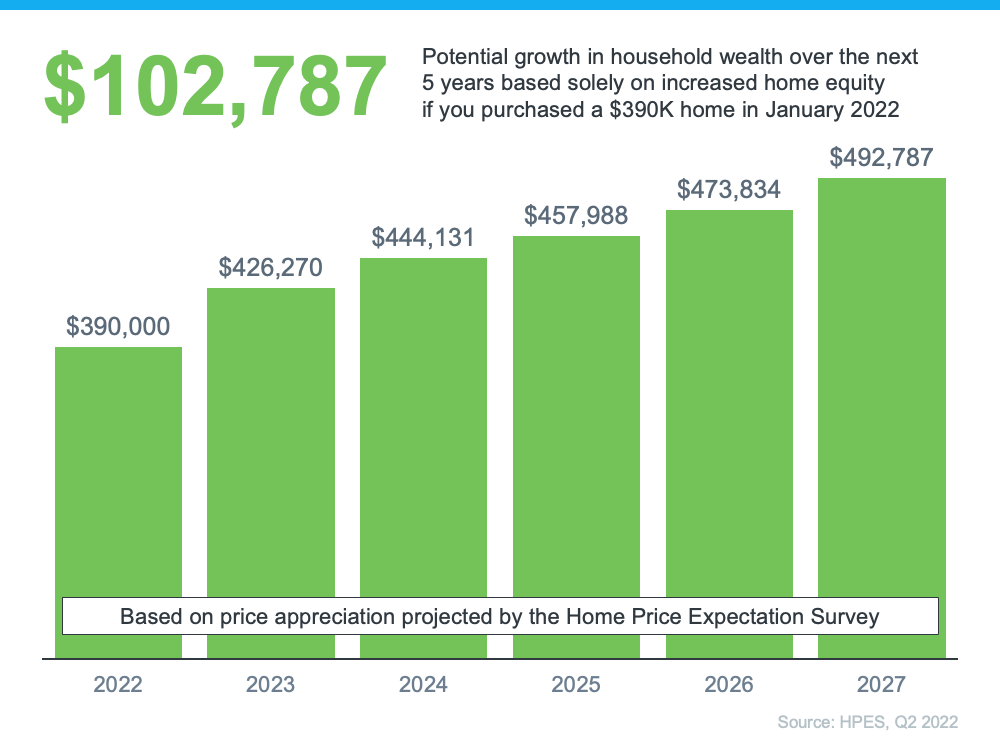

Owning real estate can positively impact your net worth. Here’s how a typical home could grow in value over the next few years using the expert price appreciation projections from the Pulsenomics survey mentioned above (see graph below):

As the graph conveys, even at a more typical pace of appreciation, you still stand to make significant equity gains as your home grows in value. That’s what’s at stake if you delay your plans.

Buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost. When you have a fixed-rate mortgage on your home, you lock in your monthly payment for the duration of your loan, often 15 to 30 years. James Royal, Senior Wealth Management Reporter at Bankrate, says:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same. That’s certainly not the case if you’re renting.”

So even if other prices increase, your housing payment will be a reliable amount that can help keep your budget in check. If you rent, you don’t have that same benefit, and you won’t be protected from rising housing costs.

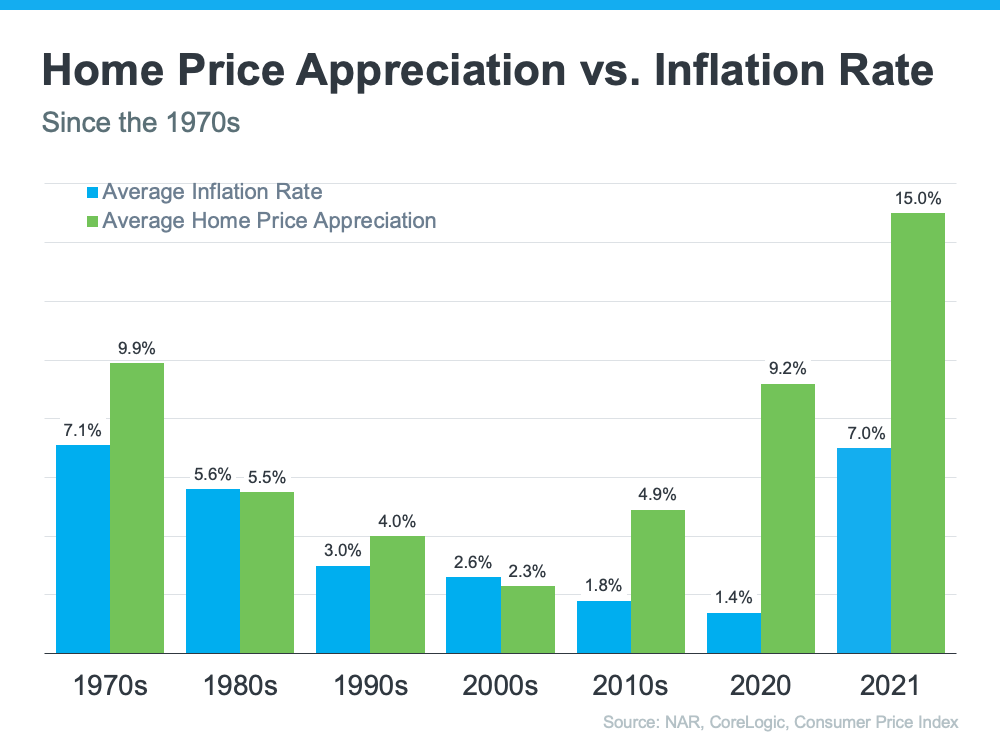

Investing in an Asset That Historically Outperforms Inflation

While it’s true rising home prices and higher mortgage rates mean that buying a house today costs more than it did even a few months ago, you still have an opportunity to set yourself up for a long-term win. That’s because, in inflationary times, you want to be invested in an asset that outperforms inflation and typically holds or grows in value.

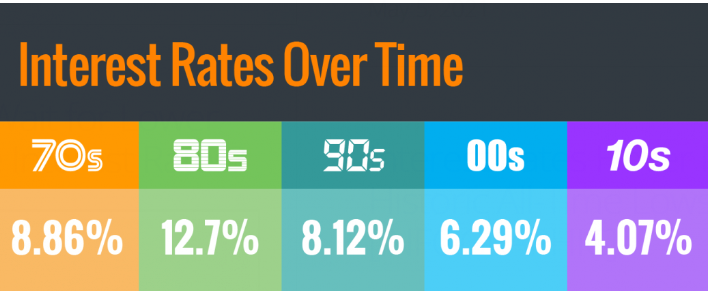

The graph below shows how the average home price appreciation outperformed the average inflation rate in most decades going all the way back to the seventies – making homeownership a historically strong hedge against inflation (see graph below):

What better way to fight inflation than to have an investment that appreciates (especially at level in line or above with inflation)? A typical savings account does not even come close with our record-breaking inflation rate of 9.1%.

Let’s Have A Conversation

If anything, now is the time for a conversation. There’s no commitment, just a friendly conversation about the real estate market, interest rates, prices, the Pikes Peak Region, or anything you might have questions about. Even if your time frame is 6-12 months out, we can help guide you in the right direction for when the time is right for you. Please contact us today!